It's been tough to swap my free time to actually write here, but I feel the need to organize my thoughts into 2013. Ray Dalio is thinking differently than me and him and his team are smart people, who do a lot of research, etc. It's late, around 11pm.

So...

Maybe I have read too much of Richard Koo.

What does he repeat on a regular basis in his pieces?

- Most of the developed world is in a balance-sheet recession.

What does that mean?

// Households and Corporates are saving in order to reduce their overall debt levels, even though interest rates are so low. The DEMAND for credit is low/negative, therefore monetary policy loses traction.

// Therefore Governments must fill the gap through public spending to keep aggregate demand supported.

Something along those lines. I'm not an academic.

Or maybe the IMF paper about "fiscal multipliers in downturns and upturns" that was so publicized recently fits the theory in my mind...

The summary says:

I read some people disregarded some of the conclusions on this paper on the basis that the current, ongoing, economic issues have a few peculiarities, etc. But I am not an academic. In my head it makes sense, just as I believe the Ibovespa has a higher Beta to the SPX on market routs than it has Beta to the SPX on market rallies. I can come up with untested reasons for that, such as lower liquidity and currency risk.

Or the psychological drag human minds have when they're depressed and take another hit. Our beloved race can't stand pain. A 'unit of happiness' has an utility value smaller than one 'unit of sadness'. Something along those lines.

So where does the EZ/UK analog from the title of this post?

The UK:

- Free-floating currency.

- BOE had massive QE program.

- The Olympic Games that happened recenly

- And the Government did some amount of marginal fiscal drag.

Eurozone:

- Pseudo-Gold standard as currency.

- ECB started out with hawkish Trichet which pulled liquidity squeezing banks/collateral values, etc... with SMP, Draghi-the-Dragon, then rate cuts, LTROs and then powerful "believe me, it will be enough" vocal chords which culminated with OMT.

- And... Fiscal Drags.

And the US:

- Free-floating currency

- Grand QE scheme

- And just NOW, a pop in fiscal drag!

So far we have the US growing more than the UK which has grown more than the Eurozone.

As I usually say: perhaps I am using statistics that please my idea/framework, but here are two charts.

The first one is of the Budget Deficits of all three mentioned, but subtracting their starting fiscal balances (end-2007), in order to normalize: "Who Boosted Spending the Most When Crisis Hit?".

And the chart already says it, the US was also the one who still runs the larger deficit of all three.

So to keep things objective: I fear for US economic activity more than the consensus. They have JUST STARTED a larger fiscal drag, from a higher fiscal deficit level. The consensus has gotten things wrongs so many times, with their dozens of econometric models, data-mining, even decades of experience, so... I read the consensus, and try to come up with reasons to agree or disagree with it. Right now I disagree. But market prices disagree with me. Or I am missing other pieces of the puzzle. Is Hussman correct? Is the ECRI correct?

A few interesting data-points:

// 4Q12 US Personal Income had a boost due to antecipated dividends which were paid to avoid higher taxation from the so-called Fiscal Cliff. If it wasn't for above-normal dividends the number, instead of +2.6%, would come in as 0.6%, in line with expectations of 0.8%.

// So now we look at US Retail Sales. Sharply revised Nov12 and Dec12 #s, very strong, just to slowdown to almost a stand-still in Jan13. Were the Nov-Dec12 #s strong due to Sandy giveback and/or this excessive antecipated jump in Personal Income due to extraordinary dividends? I don't know.

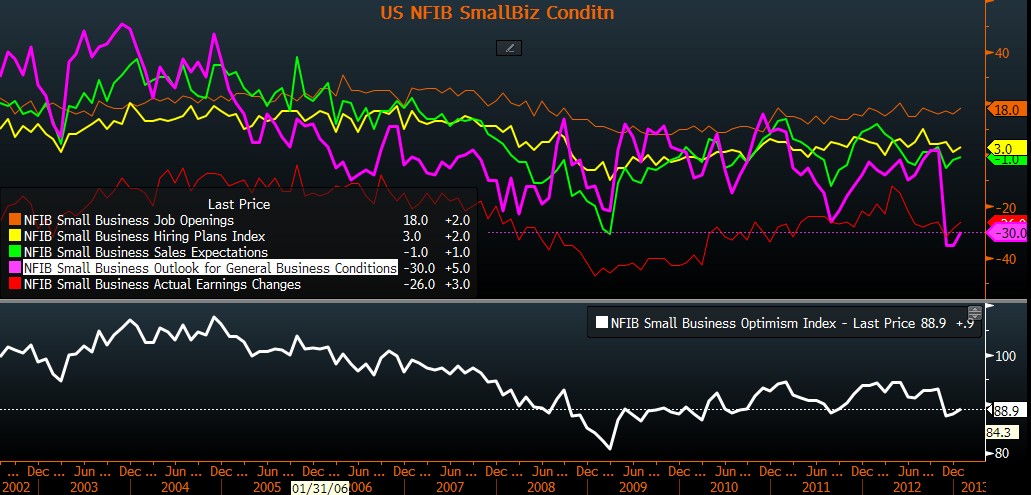

// Here's the NFIB Small Business Conditions. It's barely at the 2011-low level, dragged by "Outlook for the Economy" which made new all-time-lows and recovered a bit in the past 2 months. Hiring plans remain depressed.

// And Core Capital Goods ORDERS, coming in negative for December after 2 strong months.

So here we have, so far, a slow down in Income (possibly, check out the Taxes Withheld at the US Treasury change in trend, despite still very high levels historically), likely slower due to a) less dividends and b) the payroll tax hikes, consequently a slow down in Retail Sales and also a slow down in Employment growth, Investments?

Interesting, because if balance sheet recessions really exist and the examples of the Eurozone, or more appropriately, the UK, count... perhaps the US is just about to underperform. And we know what happens when the US underperforms. The world gets sick.

Oh, and by the way, suggestions/criticism is VERY welcome.

So...

Maybe I have read too much of Richard Koo.

What does he repeat on a regular basis in his pieces?

- Most of the developed world is in a balance-sheet recession.

What does that mean?

// Households and Corporates are saving in order to reduce their overall debt levels, even though interest rates are so low. The DEMAND for credit is low/negative, therefore monetary policy loses traction.

// Therefore Governments must fill the gap through public spending to keep aggregate demand supported.

Something along those lines. I'm not an academic.

Or maybe the IMF paper about "fiscal multipliers in downturns and upturns" that was so publicized recently fits the theory in my mind...

The summary says:

Summary: Only a few empirical studies have analyzed the relationship between fiscal multipliers and the underlying state of the economy. This paper investigates this link on a country-by-country basis for the G7 economies (excluding Italy). Our results show that fiscal multipliers differ across countries, calling for a tailored use of fiscal policy. Moreover, the position in the business cycle affects the impact of fiscal policy on output: on average, government spending, and revenue multipliers tend to be larger in downturns than in expansions. This asymmetry has implications for the choice between an upfront fiscal adjustment versus a more gradual approach.

I read some people disregarded some of the conclusions on this paper on the basis that the current, ongoing, economic issues have a few peculiarities, etc. But I am not an academic. In my head it makes sense, just as I believe the Ibovespa has a higher Beta to the SPX on market routs than it has Beta to the SPX on market rallies. I can come up with untested reasons for that, such as lower liquidity and currency risk.

Or the psychological drag human minds have when they're depressed and take another hit. Our beloved race can't stand pain. A 'unit of happiness' has an utility value smaller than one 'unit of sadness'. Something along those lines.

So where does the EZ/UK analog from the title of this post?

The UK:

- Free-floating currency.

- BOE had massive QE program.

- The Olympic Games that happened recenly

- And the Government did some amount of marginal fiscal drag.

Eurozone:

- Pseudo-Gold standard as currency.

- ECB started out with hawkish Trichet which pulled liquidity squeezing banks/collateral values, etc... with SMP, Draghi-the-Dragon, then rate cuts, LTROs and then powerful "believe me, it will be enough" vocal chords which culminated with OMT.

- And... Fiscal Drags.

And the US:

- Free-floating currency

- Grand QE scheme

- And just NOW, a pop in fiscal drag!

So far we have the US growing more than the UK which has grown more than the Eurozone.

As I usually say: perhaps I am using statistics that please my idea/framework, but here are two charts.

The first one is of the Budget Deficits of all three mentioned, but subtracting their starting fiscal balances (end-2007), in order to normalize: "Who Boosted Spending the Most When Crisis Hit?".

And the chart already says it, the US was also the one who still runs the larger deficit of all three.

So to keep things objective: I fear for US economic activity more than the consensus. They have JUST STARTED a larger fiscal drag, from a higher fiscal deficit level. The consensus has gotten things wrongs so many times, with their dozens of econometric models, data-mining, even decades of experience, so... I read the consensus, and try to come up with reasons to agree or disagree with it. Right now I disagree. But market prices disagree with me. Or I am missing other pieces of the puzzle. Is Hussman correct? Is the ECRI correct?

A few interesting data-points:

// 4Q12 US Personal Income had a boost due to antecipated dividends which were paid to avoid higher taxation from the so-called Fiscal Cliff. If it wasn't for above-normal dividends the number, instead of +2.6%, would come in as 0.6%, in line with expectations of 0.8%.

// So now we look at US Retail Sales. Sharply revised Nov12 and Dec12 #s, very strong, just to slowdown to almost a stand-still in Jan13. Were the Nov-Dec12 #s strong due to Sandy giveback and/or this excessive antecipated jump in Personal Income due to extraordinary dividends? I don't know.

// A sequential slowdown in NFP growth. I've read somewhere that Small Business are the engine of job growth.

// Here's the NFIB Small Business Conditions. It's barely at the 2011-low level, dragged by "Outlook for the Economy" which made new all-time-lows and recovered a bit in the past 2 months. Hiring plans remain depressed.

// And Core Capital Goods ORDERS, coming in negative for December after 2 strong months.

So here we have, so far, a slow down in Income (possibly, check out the Taxes Withheld at the US Treasury change in trend, despite still very high levels historically), likely slower due to a) less dividends and b) the payroll tax hikes, consequently a slow down in Retail Sales and also a slow down in Employment growth, Investments?

Interesting, because if balance sheet recessions really exist and the examples of the Eurozone, or more appropriately, the UK, count... perhaps the US is just about to underperform. And we know what happens when the US underperforms. The world gets sick.

Oh, and by the way, suggestions/criticism is VERY welcome.

*Disclaimer: charts and data are presented as I receive/see them. Sources are usually not checked for validation and my own calculations are of 'back of the envelope'-type. I am aware that some math that I do myself might be wrong and/or misleading to some extent. In financial markets the rate of change of economic data is often more important than the actual level and the perception of 'what is priced in' is more important than 'what is actually going to happen'. This is actually the way people pick entry and exit points. So... yes, sometimes you might say 'This guy is an idiot, this is way wrong!' with a high conviction, being right. Not to worry. Markets are made of expectations and the clash of conviction between its participants. Portfolio managers know that being an idiot is sometimes profitable and being smart is often a bad choice. It is all reality, sometimes good, sometimes bad. By the way: corrections to my analysis and intelligent debate is welcome. theintriguedtrader AT gmail do com

No comments:

Post a Comment